Inherited Property and Estates with Development Potential: Getting Clarity Before Decisions Are Locked In

A practical guide for beneficiaries and executors navigating developer interest, pricing logic and sale pathways in New South Wales.

The issue many beneficiaries and executors face

When an estate includes property with development potential, beneficiaries and executors often find themselves operating in unfamiliar territory. Unlike a conventional residential sale, development potential places the property in a specialised segment of the property market, with different pricing logic, risks and decision points.

At this stage, pressure can build quickly. Developers may approach the estate directly. Family members may hold different views about timing or value. Executors may feel a responsibility to “do something” while also worrying about personal liability and making decisions that cannot be unwound.

The difficulty is not a lack of good intent. It is that early choices, often made before the property is properly understood from a development perspective, can shape outcomes in ways that are hard to reverse.

Context: why development potential changes the decision making framework

Property with development potential does not behave like ordinary residential property. That distinction is critical, yet often underestimated.

A typical home buyer looks at comparable sales, personal preferences and borrowing limits. A developer approaches the same property very differently. Their starting point is an assumed development outcome. They test planning controls, site constraints, likely yield, construction cost, finance cost, risk allowances and profit requirements. Only then do they work backwards from project gross revenue to determine what they can justify paying for the land.

This means two important things for estates:

The property’s appeal and pricing are driven by development feasibility, not emotional or lifestyle value.

Development potential is not always obvious without targeted analysis. What looks promising on the surface may be constrained in ways that materially affect value, risk or buyer appetite. Equally, what looks unfavourable may not be.

Crucially, potential does not equal certainty. Planning pathways, approval discretion, design quality and market conditions all matter, particularly in New South Wales where planning controls and assessment outcomes can vary significantly by location and proposal.

Analysis: where incomplete knowledge creates risk

Most problems arise not from poor advice but from decisions being made before the right questions are answered.

Acting on assumptions rather than evidence

Beneficiaries and executors often inherit assumptions along with the property: “it’s zoned for apartments,” “developers are active in the area,” or “we should combine it with the neighbours.” Some of these may be partially true. None are reliable enough on their own to guide a sale strategy.

Without an informed view of what a realistic development might look like, it is difficult to assess whether developer interest is genuine, opportunistic or conditional on assumptions that may not hold.

Engaging too early with developers

A direct approach from a developer is not unusual. It can be a useful signal that the property is potentially attractive to the development market. But it is also usually an attempt to secure control of the site early, without competition and on terms that suit the developer.

Early pricing conversations, heads of agreement or exclusivity arrangements can materially narrow options before the estate understands what it is agreeing to. These steps are often framed as non-binding but can still affect leverage and future negotiating position.

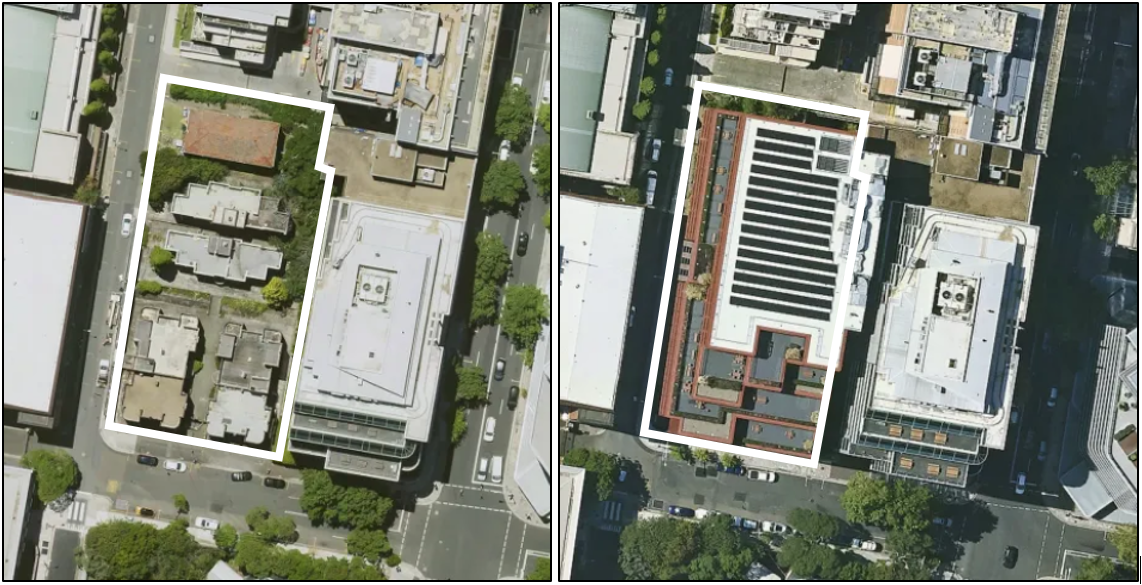

Before and After Development

Locking into a sale pathway prematurely

Choosing an agent, committing to a particular sale method, or negotiating in isolation can become de facto commitments. Once an estate embarks on a path, changing course can be difficult, commercially, legally and within family dynamics.

For executors in particular, this sequencing matters. Early decisions can expose the estate, and sometimes the executor personally, to criticism or dispute if beneficiaries later question why alternatives were not explored.

How developers actually assess and price sites

Understanding how developers think does not require becoming a developer. It does require clarity on a few fundamentals.

Developers assess sites by reference to feasibility, not market sentiment. This includes:

the likely development form supported by planning controls and constraints,

site efficiency, access, services and buildability,

risk factors that affect approval, delivery and timing,

capital costs, finance assumptions and required contingency, and

the margin required to justify proceeding.

Comparable sales may play a role, but usually as a check rather than a driver. Two sites with similar zoning can attract very different pricing depending on expected gross revenue, shape, access, servicing, constraints and risk profile. This is why development potential is not always apparent, even to experienced property owners.

Importantly, this type of analysis is not a valuation and does not predict an approval outcome. It is a way of understanding how the market is likely to think about the site, and why offers may differ in structure, timing and conditions.

Implications for beneficiaries and executors

Once it is recognised that this is a specialised market, several practical implications follow.

Firstly, information asymmetry matters. Developers typically operate with more information and experience than estates encountering this market for the first time. That imbalance influences pricing, terms and negotiation dynamics.

Secondly, early decisions can have long lasting effects. Engaging with one party, ruling out others or accepting restrictive terms can close options before they are properly tested.

Thirdly, independence matters. Advice that is aligned solely with the landowner, rather than a prospective buyer or a transaction outcome, has its greatest value before the sale path is chosen.

For executors, this can be particularly important. Independent commercial and strategic guidance can help demonstrate that decisions were made with reasonable care, proper sequencing and an understanding of risk, rather than under pressure or based on assumption.

What “early clarity” actually looks like

Early clarity does not mean committing to a sale, pursuing development or spending heavily on project schemes or legal documentation. It means answering a defined set of questions before decisions become difficult to unwind, including:

What plausible development outcomes could the site support in principle?

Which constraints are likely to matter most to developers?

How would a developer broadly think about feasibility and risk here?

What types of buyers would realistically see value in the site?

What sale or negotiation pathways are available and what do they involve?

This form of guidance is commercial and strategic rather than legal or valuation advice. It does not determine outcomes. It improves the quality of decisions by replacing assumption with understanding.

Practical insight: sequence before commitment

The single biggest mistake owners of property with development potential make is failing to recognise that they have entered a specialised subsector of the market, and then acting too quickly based on incomplete knowledge.

For beneficiaries and executors, the practical lesson is simple but significant. Before engaging agents, entering negotiations or selecting a sale method, it is worth pausing long enough to understand:

how this market actually works,

how developers are likely to assess and price risk, and

what options genuinely exist before any one path is locked in.

That early step keeps future options open. It reduces unnecessary risk, particularly where family interests or executor responsibilities are involved. Most importantly, it allows decisions to be made deliberately, rather than in response to pressure.

In estates involving development potential, clarity before commitment is not a delay. It is a form of risk management.